Fake Precious Metal Certificates and Credit Risks

Precious metals like gold, silver, platinum, and palladium are considered safe havens for investors. They have intrinsic value, global liquidity, and centuries of trust behind them. Yet even this market has its weak points, and one of the biggest is paperwork. Certificates of authenticity are the backbone of metal transactions, especially in large-volume trades. They assure buyers and lenders that bars, coins, or collections are genuine. But fake certificates have become increasingly common, creating hidden risks—particularly when loans are involved. A forged document can turn a secure investment into an unsecured liability. For investors borrowing to enter the metals market, verifying certificates is not just about avoiding fraud, it is about protecting themselves from long-term financial exposure.

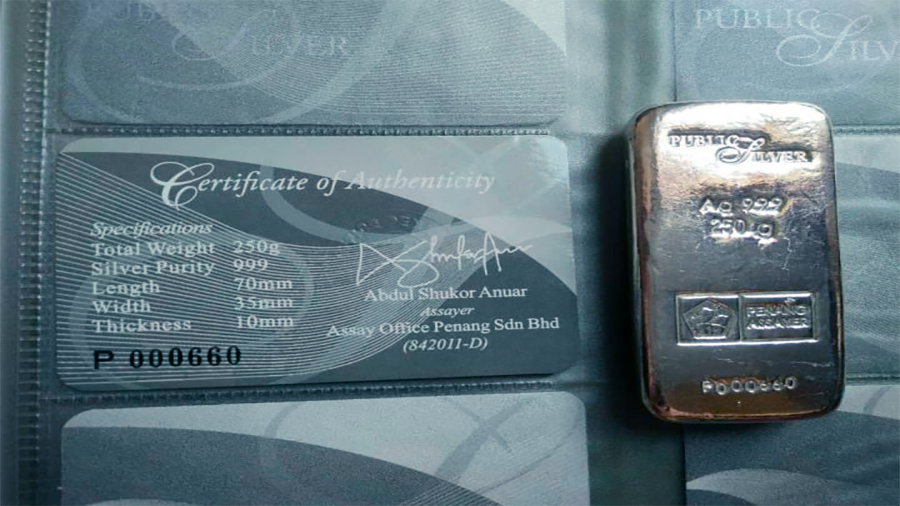

Why Certificates Matter in Metal Transactions

Precious metals are difficult to distinguish once refined. A one-kilogram bar of gold looks much the same whether pure or diluted with alloys. Certificates step in to provide critical information: purity, weight, refinery origin, and serial numbers. These details are essential when using metals as collateral for loans. Banks, private lenders, and investment funds all depend on these certificates to calculate value and assess risk. If a certificate is fraudulent, the borrower may be holding an asset that does not match the claimed specifications. For lenders, this turns secured loans into unsecured debt overnight. Certificates, in other words, are the paperwork equivalent of a lock on the vault. When they are fake, both the lock and the vault are compromised.

Elements of a Precious Metal Certificate

| Element | Purpose | Risk if Fake |

|---|---|---|

| Issuer name/logo | Confirms responsible refinery | False branding hides counterfeit origin |

| Serial number | Links document to specific bar/coin | Duplicated or reused across forgeries |

| Weight and purity | Defines financial value | Borrower overpays for diluted metal |

| Security features | Holograms, QR codes, seals | May look real but fail digital validation |

How Fake Certificates Create Credit Risks

Using borrowed funds magnifies the danger of fraudulent certificates. When investors buy metals with loans, they rely on documents to confirm that the purchase is sound. If a certificate is fake, the borrower is left with debt tied to metals worth far less than expected. Lenders, too, face loss: if repayment fails, repossessing the collateral does not cover outstanding balances. Fake certificates therefore create systemic risk. They erode confidence in collateralized lending, spark legal disputes, and slow down financial flows in global trade. For international deals, where jurisdictional differences already complicate enforcement, a fraudulent certificate can drag disputes across borders for years. The financial damage extends well beyond a single investor or lender; it undermines trust in the metals sector itself.

Verification Practices That Reduce Exposure

Preventing fraud requires more than a quick glance at paperwork. Modern verification uses layers of checks, combining traditional documentation with digital tools. Investors can confirm an issuer’s legitimacy by checking refinery registries. Serial numbers should be cross-referenced with official databases. Independent assay tests can confirm purity and weight, ensuring the certificate matches physical reality. Increasingly, blockchain systems are being introduced, allowing certificates to be logged in immutable digital ledgers. QR codes linked to official databases offer real-time checks that can be performed by both buyers and lenders. Borrowers presenting verified certificates gain credibility and often access better loan terms, while lenders reduce their exposure to nonperforming loans.

Steps for Certificate Verification

| Step | How It Works | Benefit |

|---|---|---|

| Issuer registry check | Validate refinery in accredited list | Filters out fake companies |

| Serial number cross-check | Match with official databases | Reveals duplicates or reused IDs |

| Independent assay | Physical testing of purity and weight | Confirms certificate accuracy |

| Digital scan | QR codes or blockchain-linked proofs | Fast verification of authenticity |

Stakeholder Perspectives

Borrowers

For investors using loans, fake certificates create debt without reliable collateral. A borrower who unknowingly accepts fraudulent paperwork faces repayment pressure even if the underlying asset loses most of its value. By insisting on verified documents, borrowers not only protect themselves but also strengthen their credibility in the eyes of lenders. Verified collateral means better interest rates and more flexible loan terms.

Lenders

Banks and credit institutions cannot afford to hold counterfeit-backed collateral. They increasingly require independent verification before releasing funds. In many cases, lenders hire third-party specialists to confirm both certificates and physical assets. This extra step increases transaction time but saves far more in avoided losses. For lenders, certificate verification is as important as credit scoring.

Regulators

Market regulators recognize that fake certificates destabilize trust in financial systems. They push for stronger verification standards, encourage blockchain solutions, and impose penalties on institutions that fail to perform proper checks. Regulators see this as more than an investor problem; it is a systemic issue with implications for global trade and financial security.

Mini-Scenarios of Risk and Prevention

The Corporate Buyer

A trading company uses a loan to purchase silver bars for resale. Certificates appear genuine but later prove to be duplicated across multiple shipments. The company faces repayment pressure with assets worth only a fraction of the borrowed amount. By failing to cross-check serial numbers, both the borrower and the lender fall into a trap that could have been avoided with simple database verification.

The Private Collector

An individual investor secures financing to buy a set of platinum coins at auction. Verification later reveals that the certificates came from a non-accredited issuer. The metals are real but less pure than claimed. The collector is left paying off a loan on assets worth 30% less than expected. A basic refinery registry check would have flagged the problem before purchase.

The International Lender

A bank finances a cross-border deal involving gold bars. Months later, legal disputes arise after an independent assay shows mismatched purity levels compared to the certificates. The bank must absorb part of the loss because it released funds before conducting independent tests. This scenario highlights how lenders share responsibility for certificate verification, not just borrowers.

Forward-Looking Developments

The next decade will likely reshape certificate verification. Blockchain registries are already being tested by major refineries, offering unalterable ownership records. Artificial intelligence may soon detect anomalies in certificate design, serial number usage, or issuer patterns across global markets. Some regulators are considering mandating digital certificates only, eliminating paper documents vulnerable to forgery. Borrowers may one day present digital tokens linked directly to refinery-issued records when seeking loans. Lenders, in turn, will integrate instant verification into credit platforms, approving funds only when authenticity is confirmed. Fraud will never vanish completely, but these innovations will make fake certificates far harder to use.

Conclusion

Fake precious metal certificates pose real and growing credit risks. They trap borrowers in debt tied to undervalued assets, expose lenders to unsecured loans, and erode confidence in global markets. Verification practices—issuer checks, serial number reviews, assays, and digital scans—offer effective protection, but only if consistently applied. Mini-scenarios demonstrate how different actors can suffer or succeed depending on their diligence. Looking ahead, digital systems and blockchain tools will likely dominate verification, making fraud harder but not impossible. For anyone borrowing to buy metals, the rule is simple: never trust a certificate at face value. In the high-value world of precious metals and loans, authenticity is the only safeguard worth paying for.